The Fed just dropped another hint about rate hikes. According to their latest minutes, most FOMC members think we could see another bump if inflation stays stubborn. For small businesses already dealing with tighter cash and slower-paying clients, this timing couldn't be worse.

I've watched businesses scramble through three rate cycles now. Same thing happens every time — everyone waits too long to adjust their invoicing. By the time they realize their terms aren't working anymore, they're bleeding cash.

It's not just that money costs more when rates go up. Your entire cash conversion cycle slows down. Clients take longer to pay because their credit lines cost more. Your bank charges higher fees on everything. That vendor who used to give you 60 days suddenly wants payment in 30. Meanwhile, you're still operating with the same net-30 terms you've used since 2019.

The hidden math of rising rates on receivables

Say you invoice $40,000 a month with standard net-30 terms. In a normal rate environment, maybe 70% pays on time, 20% pays within 45 days, and 10% stretches to 60+ days. Your average collection period sits around 38 days.

When rates jump, that portfolio shifts. Now only 55% pays on time. Another 30% pushes to 45 days, and 15% goes past 60. Your average collection jumps to 47 days. That extra 9 days means you're floating an additional $12,000 in working capital at all times.

If you're borrowing against receivables at prime plus 3%, and prime jumps from 8% to 9.5%, that extra float costs you roughly $2,100 more per year. But that's just the direct cost.

The real damage comes from what you can't do because your cash is tied up. A marketing agency I worked with last year learned this the hard way. They had about $280,000 in monthly billings, mostly net-45 terms for enterprise clients. When rates started climbing, their average collection stretched from 52 days to 71 days. They had to turn down three new projects because they couldn't float the upfront costs while waiting for payment. Lost opportunity: around $85,000 in margin.

They could have prevented most of it by adjusting their invoicing structure six months earlier.

Change #1: Shorten your payment windows selectively

Not all clients deserve the same terms anymore. The knee-jerk reaction is to move everyone to net-15 or demand immediate payment, but that usually backfires.

Stop chasing payments and start automating your billing.

Billoly empowers you to create, send, and track invoices effortlessly while maintaining professional client relationships.

- Customizable invoice templates

- Automated payment reminders

- Real-time payment tracking

No credit card required

Instead, segment your client base by payment history and relationship value. Your tier-one clients — the ones who've paid on time for over a year and represent significant revenue — keep their current terms. Maybe even extend them slightly as a loyalty play. These relationships are worth protecting.

New clients get net-15 with a 2% early payment discount for payment within 5 days. This filters out clients who are already cash-strapped while incentivizing quick payment from those who can afford it.

The middle tier is where you make surgical adjustments. Clients who regularly pay 10-15 days late get moved from net-30 to net-20. Those who push past 45 days drop to net-15 or require deposits.

One approach that works surprisingly well: offer clients a choice between shorter terms with a discount or current terms at full price. About 40% will take the discount, improving your cash position without damaging relationships.

Change #2: Implement staged deposit requirements

Deposits used to be for risky clients. Now they're for managing cash flow during uncertain rate environments. But asking for 50% upfront on everything screams desperation.

| Project Size | Established Clients | New Clients |

|---|---|---|

| Under $5,000 | No deposit | 25% deposit |

| $5,000 - $15,000 | 25% deposit | 35% deposit |

| Over $15,000 | 35% upfront, 35% midpoint, 30% completion | 50% upfront, 30% midpoint, 20% completion |

For new clients, add one tier to whatever they'd normally hit. A $3,000 project needs 25% down. A $8,000 project needs 35%.

Frame this as project insurance, not mistrust. "With financing costs increasing across the industry, we're implementing milestone-based invoicing to ensure uninterrupted project delivery for all our clients."

A web development shop in Austin made this shift last fall. They went from floating an average of $43,000 in project costs to about $18,000. The freed-up capital let them take on two additional projects per month.

Change #3: Add explicit late payment escalation triggers

Vague late payment fees don't work when money is expensive. Your terms need automatic escalation with specific triggers and consequences.

Here's a framework that actually gets results:

-

Day 1-5 late

Friendly reminder, no fee

-

Day 6-15 late

1.5% fee, pause on new work

-

Day 16-30 late

Additional 2% fee, total pause on all work

-

Day 31+ late

Monthly 3% compound fee, formal collection notice

The critical part — you need to communicate these triggers before they hit. Send a pre-notice at day -5, explaining exactly what happens if payment doesn't arrive. Most clients will pay just to avoid the hassle.

The escalation needs teeth though. Actually pause work. Actually add the fees. Actually send to collections. Once clients realize you're serious, payment behavior changes fast.

Change #4: Restructure service agreements with rate adjustment clauses

For recurring revenue businesses, your service agreements need language that lets you adjust payment terms when base lending rates move more than 2% in either direction. Don't bury this in small print.

Make it a discussion point during renewal conversations. "We're adding flexibility clauses to help both parties adapt if the economic environment shifts significantly."

-

If prime rate increases 2% from contract date, payment terms shorten by 10 days

-

If prime rate increases 3%, monthly retainers require 15% deposit for the following month

-

If prime rate decreases 2%, payment terms can extend back to original

A fractional CFO service I know added these clauses to all renewals starting in January. When rates jumped in March, they were able to adjust terms on 40 clients without a single dispute. The clients understood because the triggers were objective and disclosed upfront.

The key is transparency. Nobody likes surprises when their payment terms change.

Change #5: Create payment plan options before they're needed

When rates are high, clients who used to pay in full start asking for payment plans. If you wait until they ask, you're negotiating from weakness.

Build the options now. Offer three standard plans:

-

Full payment with 3% discount

-

Two payments (50% up front, 50% in 30 days) at standard price

-

Three payments (40%, 35%, 25% over 60 days) with 4% financing fee

The financing fee is key. It needs to cover your actual cost of capital plus margin for the risk. Right now, that's probably 8-12% annually, so 4% for a 60-day plan is reasonable.

Present these options proactively on larger invoices. "We offer flexible payment options to help manage cash flow" sounds better than scrambling when a client can't pay.

Change #6: Move retainer clients to prepayment with incentives

Monthly retainers are great until clients start paying them late. The fix isn't chasing payment — it's eliminating the chase entirely.

Transition retainer clients to prepayment by offering a meaningful incentive. A 5-7% discount for quarterly prepayment usually works. For a $4,000 monthly retainer, that's $200-280 off per quarter.

Most clients jump at it. The math works because you eliminate collection costs, reduce receivables risk, and can deploy that capital immediately. Even after the discount, you come out ahead.

Start with your best clients. Once a few switch, others follow. Within six months, you can convert 60-70% of retainer revenue to prepayment.

For those who won't prepay, require auto-billing on a credit card with a backup card on file. This connects naturally to systematic retainer structures that protect cash flow through multiple payment methods.

Change #7: Build interest-bearing escrow into large projects

For projects over $25,000, consider requiring escrow funding rather than traditional invoicing. The client funds an escrow account that releases payments at predetermined milestones.

This sounds extreme, but it's becoming standard in professional services. The client's money sits in an interest-bearing account they control. You get guaranteed payment at milestones. Both parties are protected.

An architectural firm started doing this for commercial projects last year. Their receivables dropped by 60%, and they haven't had a single payment dispute since.

Clients actually prefer it because it simplifies their accounting. No more tracking outstanding invoices or managing cash flow for project payments. Everything is funded upfront and released automatically.

The operational reality of rate-sensitive invoicing

Making these changes isn't just about updating your terms and conditions. You need operational workflows that can actually execute them.

Your invoicing system needs to track multiple payment term tiers, automatically calculate early payment discounts, and trigger escalation sequences without manual intervention. Most small businesses try to manage this in spreadsheets, which breaks down fast when you have 30+ clients on different terms.

Think about the daily workflow. Someone has to check which invoices are approaching late fees, calculate pro-rated penalties, send pre-notices, and pause services when triggers hit. If you're doing this manually for 50+ invoices, it's eating hours every week.

AI-powered operational software starts making sense here. Instead of manually tracking which client is on which terms, when to send reminders, and calculating pro-rated fees, you build the rules once and let automation handle the execution. A platform that understands your client segments can automatically adjust terms based on payment history, send pre-notices before late fees kick in, and even pause service access when payments hit certain thresholds.

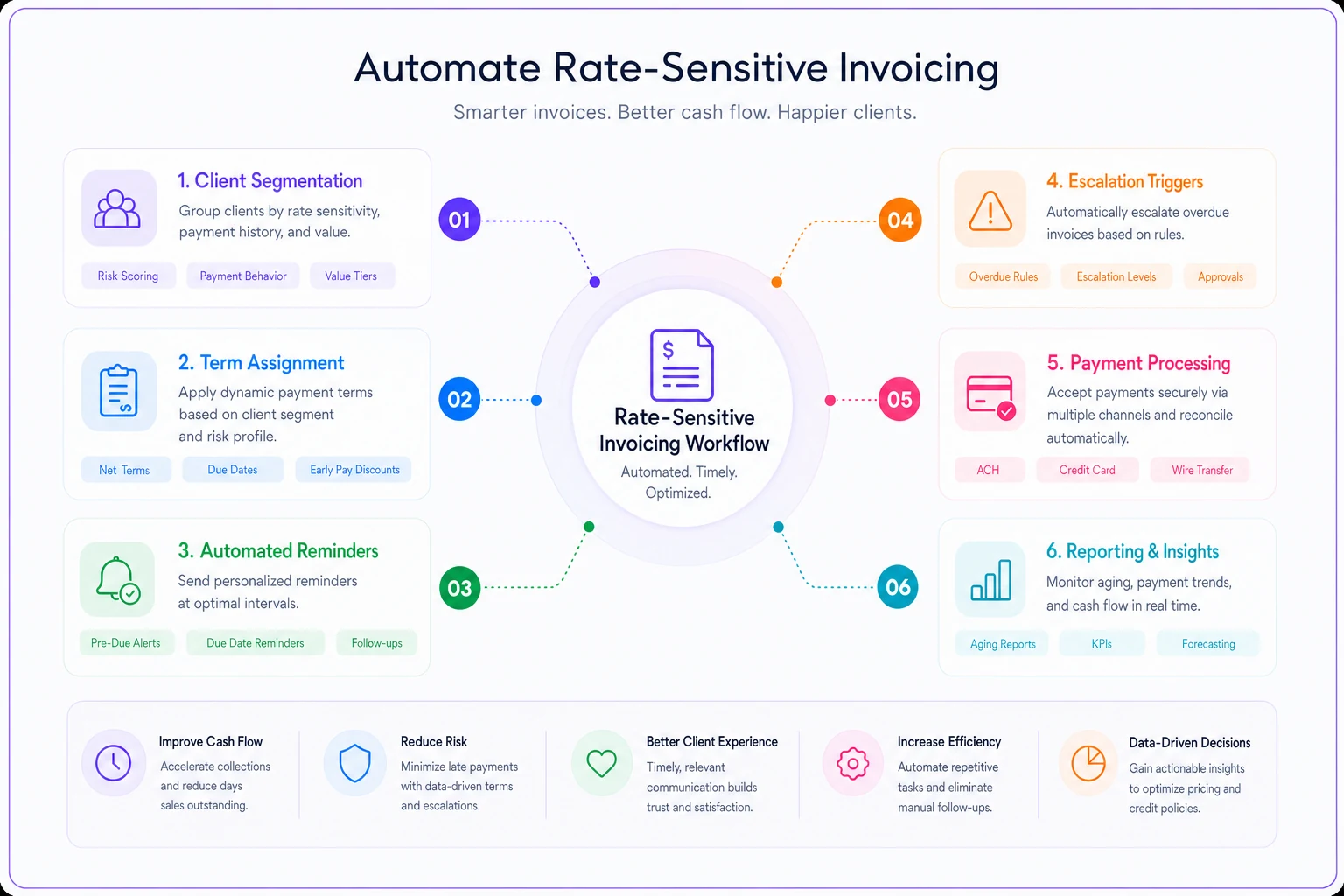

Here's a workflow to implement these operational changes.

This visual outlines how automation ties the steps together.

The real value isn't replacing human judgment — it's freeing your team from repetitive tracking tasks so they can focus on client relationships and exception handling.

Making the shift without losing clients

The biggest fear around tightening invoicing terms is client backlash. But structured correctly, most clients won't just accept the changes — they'll appreciate the transparency.

Start by grandfathering your top 20% of clients for 90 days. Send them a personal note explaining the changes and that you're protecting them from immediate impact. This builds goodwill and prevents your biggest revenue sources from shopping around.

For everyone else, provide 60 days notice with clear explanation of the macroeconomic factors driving the change. CNBC's coverage of the Fed minutes gives you third-party validation that rates might climb further.

Roll out changes in waves. Week 1: new clients. Week 3: clients with payment issues. Week 5: standard clients. Week 8: premium clients (if needed). This prevents your team from being overwhelmed with questions and lets you adjust based on early feedback.

Most clients understand that business conditions change. What they don't understand is sudden changes without explanation or retroactive policy shifts.

The next 90 days matter more than the next year

Rising interest rates create a cascade effect that hits small businesses from multiple angles. Your vendors tighten terms while your clients stretch payments. Your credit lines cost more while your cash needs increase.

It's a squeeze that gets worse gradually, then suddenly. The businesses that adapt their invoicing now — before the next rate hike — will have the cash flow flexibility to survive the squeeze. Those that wait will find themselves choosing between growth and survival.

Start with one change. Pick the lowest-friction adjustment that fits your business model. Maybe it's adding early payment discounts, or requiring deposits on new clients, or moving just your problem accounts to shorter terms.

Once that first change is operational, add another. Then another. By the time rates actually increase, you'll have a resilient invoicing system that protects cash flow regardless of what the Fed decides.

The goal isn't to predict exactly when rates will rise or by how much. It's to build invoicing operations that work whether rates go up, down, or sideways. Because one thing we learned from the last three years — assuming stability is the riskiest position of all.

Ready to streamline your billing process?

Join 5,000+ businesses using Billoly to reduce billing delays, automate payments, and grow revenue efficiently.