Most solopreneurs obsess over their bank balance but have zero clue what it'll look like next month. They memorize every outstanding invoice, yet cash still catches them off guard. This isn't about math skills—it's about treating invoices like paperwork instead of cash predictors.

The invoice-to-cash reality gap that keeps solopreneurs guessing

Your invoices already contain the data you need to forecast cash flow accurately. The trick is pulling out the right metrics and running them through something simple enough for weekly updates but smart enough to catch meaningful patterns.

After working with operational systems across hundreds of service businesses, the divide is obvious: companies tracking invoice aging with payment behavior spot cash problems weeks early. Everyone else scrambles for emergency funding or passes on growth because they can't predict their runway.

Why standard accounting reports fail solopreneurs

Your accounting software shows aged receivables. Maybe it even makes pretty charts. But those reports treat invoices as paid/unpaid switches. Real life is messier.

Stop chasing payments and start automating your billing.

Billoly empowers you to create, send, and track invoices effortlessly while maintaining professional client relationships.

- Customizable invoice templates

- Automated payment reminders

- Real-time payment tracking

No credit card required

That $10,000 invoice due in 15 days hits differently when the client historically pays 20 days late versus someone who sends partial payments starting day 5. Standard reports treat both situations the same until money shows up.

The model most solopreneurs actually need sits between daily bank checking and monthly P&L reviews. It has to capture payment speed, not just payment status. Promised dates matter more than due dates. Partial payments become signals, not exceptions.

Your brain already tracks these patterns if you pay attention. That client who always pays exactly 12 days late. Another sends 50% immediately then disappears for months. A third promises new dates then hits them perfectly. Your cash forecast should capture this too.

The three invoice metrics that actually predict cash

Payment velocity scoring

Every client has payment DNA. Some pay like clockwork on day 28. Others spray random partials across 60 days. Others ghost then pay everything after one reminder.

-

Average days to first payment

-

Average days to full payment

-

Partial payment frequency

-

Response time to reminders

One landscaping business discovered commercial clients averaged 42 days to payment while residential hit 18 days consistently. That insight alone let them adjust service mix to smooth cash flow without borrowing.

Promise date reliability

When a client says "I'll pay next Friday," what does that mean for your cash flow? Depends entirely on their promise track record.

-

Promises kept on time

100%

-

Promises kept within 3 days

75%

-

Promises kept within 7 days

50%

-

Promises missed

0%

Weight recent promises heavier. Someone who missed three promises six months ago but nailed the last five deserves better scoring than straight averaging.

Partial payment patterns

Partials feel like progress but often signal cash problems—yours or theirs. The pattern matters more than amounts.

-

Scheduled (milestone-based)

-

Voluntary (client-initiated)

-

Negotiated (after follow-up)

-

Defensive (dispute-related)

Clients sending voluntary partials usually have cash awareness and will finish paying. Ones sending defensive partials after multiple reminders probably won't pay the rest without escalation.

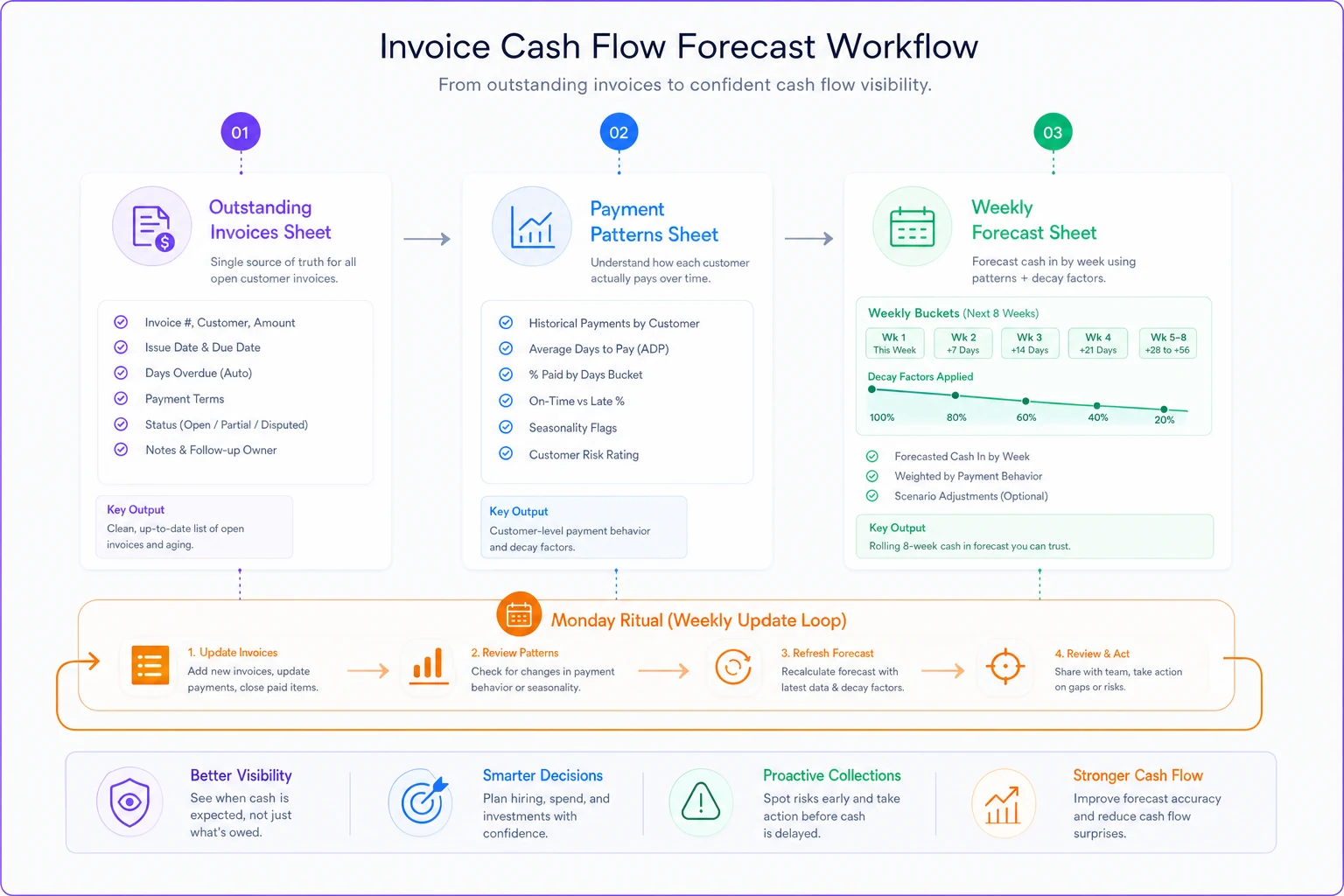

Building your weekly forecast model

Start with a simple spreadsheet. Three sheets: Outstanding Invoices, Payment Patterns, Weekly Forecast.

Outstanding Invoices sheet

| Invoice # | Client | Amount | Due Date | Promise Date | Partials Received | Status |

|---|---|---|---|---|---|---|

| INV-001 | ABC Co | $5,000 | Jan 15 | Jan 20 | $2,000 | Active |

| INV-002 | XYZ LLC | $3,500 | Jan 10 | - | $0 | Overdue |

Add columns for aging brackets (0-30, 31-60, 61-90, 90+) calculated from due date. Add another for days since last client contact.

Payment Patterns sheet

| Client | Avg Days to Pay | Promise Reliability | Partial Pattern | Last 3 Payments |

|---|---|---|---|---|

| ABC Co | 22 | 85% | Scheduled | 18, 24, 21 days |

| XYZ LLC | 45 | 60% | Negotiated | 41, 52, 44 days |

Update monthly. Weekly is overkill unless you're invoicing the same clients repeatedly within short windows.

Weekly Forecast sheet

Create 8 weekly buckets. For each outstanding invoice, calculate payment probability per bucket:

-

Week 1

Due this week + overdue promises + highly reliable near-term promises

-

Week 2

Due next week + promises adjusted for reliability

-

Week 3-4

Mix of due dates and historical patterns

-

Week 5-8

Pure historical patterns

Apply collection decay factors:

-

0-30 days

95% collectible

-

31-60 days

85% collectible

-

61-90 days

70% collectible

-

90+ days

40% collectible

Most AI-powered operational software can automate these calculations and pattern tracking. The software learns client payment behaviors automatically and adjusts forecasts based on your actual collection history rather than generic industry averages.

A simple diagram of those three sheets and the weekly update loop helps you visualize the process.

The Monday morning cash flow ritual

Block 20 minutes every Monday. Same time, same process. Consistency beats perfection.

1. Seven-minute invoice review

Export all outstanding invoices. Note payments received since Friday. Flag invoices crossing aging thresholds. Record new promise dates from client communications.

2. Five-minute pattern update

Update payment velocities for cleared invoices. Adjust promise reliability scores. Note partial payment activity. Flag pattern changes—clients paying slower or faster than usual.

3. Five-minute forecast adjustment

Redistribute invoice probabilities across weekly buckets. Apply collection decay to aging invoices. Sum expected cash by week. Compare to last week's forecast versus actual.

4. Three-minute action triggers

Check if any invoice hit 45 days. Note if any client reliability dropped below 50%. See if Week 2 forecast fell below operating expenses. Verify Week 4 forecast stays above comfort threshold.

Use a saved email template for common follow-ups to shave minutes off the ritual.

The power isn't complex modeling. It's consistent observation of how your specific clients actually pay you.

Converting fuzzy promises into forecast probabilities

"The check's in the mail" means nothing. "I'm processing this through our next AP run on the 15th" means everything. Learning to extract real commitment from payment conversations directly improves forecast accuracy.

When following up on invoices, get specific:

-

Not "when will you pay?" but "what's your AP schedule?"

-

Not "can you pay this week?" but "can you process this by Thursday for Friday payment?"

-

Not "is there a problem?" but "what do you need from me to process this?"

One web designer started asking clients to screenshot their AP dashboard showing the invoice queued for payment. Forecast accuracy jumped from 60% to 85% within a month. Clients who couldn't provide screenshots reliably paid late.

Track promise specificity:

-

Vague promises ("soon," "next week," "working on it"): 25% reliability

-

Date promises ("by Friday," "on the 15th")

50% reliability

-

Process promises ("in Thursday's check run," "wire initiating tomorrow"): 75% reliability

-

Evidence promises (screenshot, payment confirmation number)

90% reliability

When you can attach a probability to promise specificity, your weekly buckets become far more realistic.

Reading early warning signals in payment behavior

Payment changes rarely happen suddenly. Clients broadcast cash flow stress through invoice interactions weeks before missing payments entirely.

Velocity slowdown pattern: A client who consistently paid at 21 days starts hitting 28, then 35. They're managing cash flow actively, paying you slowly enough to preserve the relationship. You have maybe 60 days before they disappear.

Communication dodge pattern: Response time to your emails stretches. They stop answering calls. When they do respond, it's after hours or weekends. They're avoiding conflict, which means avoiding payment.

Partial payment probe pattern: Suddenly offering partials on invoices they previously paid in full. They're testing your boundaries. Accept without pushback and partials become their new normal.

Dispute creation pattern: Questioning charges they previously accepted. Requesting documentation for work completed months ago. Manufacturing reasons to delay payment while appearing cooperative.

Operational software with AI automation can track these behavioral shifts automatically, flagging clients showing early warning signs before you notice the patterns manually.

Adjusting your model for seasonal patterns

Most solopreneurs have predictable cash flow seasonality they completely ignore in forecasting. December payments arrive in January. August checks get lost in vacation schedules. Tax season disrupts everything.

December invoices: Add 10 days to payment velocity

August invoices: Add 7 days to payment velocity

March/April invoices: Add 5 days for corporate clients (tax season)

January invoices: Subtract 5 days (companies clearing year-end payables)

A freelance marketer noticed agency clients paid December invoices in 34 days versus 22 days normally. Adding that seasonal factor to her forecast eliminated the annual January cash crunch.

Track your own patterns across a full year. The adjustments will surprise you.

Stress-testing your forecast against reality

Your forecast will be wrong. The question is whether it's usefully wrong or dangerously wrong.

Every week, compare forecast to actual:

-

Which clients surprised you?

-

Which direction did you miss (optimistic/pessimistic)?

-

Which week buckets were most accurate?

-

What signals did you ignore?

Aim for 70% accuracy in Week 1-2, 50% accuracy in Week 3-4. Beyond that is educated guessing anyway.

When forecast consistently runs optimistic, you're probably ignoring aging reality, overweighting promises, missing behavior changes, or forgetting seasonality.

When forecast consistently runs pessimistic, you're probably undervaluing client relationships, missing partial payment signals, ignoring collection effectiveness, or forgetting recurring patterns.

Building forecast confidence without complex models

The trap many fall into is adding complexity when simple models miss. More variables rarely help. Better observation usually does.

A cleaning service owner tracked 47 different metrics trying to predict payment. Accuracy never broke 60%. She simplified to just three—days since invoice, client payment history, and promise specificity—and hit 75% accuracy consistently.

Your forecast needs enough sophistication to catch patterns, not enough to model every edge case.

Focus energy on clean invoice data, consistent client patterns, specific promise extraction, and weekly observation rhythm.

Skip complexity like multi-variable regression, industry payment benchmarks, macro-economic adjustments, or credit score integration.

Operational adjustments that flatten cash waves

Once you can forecast cash flow from invoices reliably, you can start smoothing the waves. The forecast shows you where to intervene.

-

Invoice timing optimization

If Week 3 always runs thin, shift some invoice dates earlier. Bill at 80% completion instead of 100%. Move recurring invoices from month-end to mid-month.

-

Collection effort allocation

Focus collection energy on invoices most likely to pay. That 90-day invoice from a client with 30% promise reliability? Stop wasting time. The 35-day invoice from your reliable-but-slow client? One gentle nudge probably releases payment.

-

Payment term negotiation

Offer 2% early payment discount to clients who typically pay at 30 days. They'll often take it, pulling cash forward two weeks. Add late fees to chronic slow payers. They won't pay them, but it creates urgency.

-

Partial payment strategizing

When forecast shows trouble in Week 2, proactively offer partial payment plans to your largest outstanding invoices. Better to collect 50% on schedule than 100% eventually.

The forecast helps prioritize which of these levers to pull and when.

The compound value of forecast discipline

Running this model weekly feels tedious at first. After a month, it becomes automatic. After a quarter, you'll predict client payments before they decide to send them.

The real value isn't avoiding surprises—it's making better operational decisions. You'll confidently take projects knowing cash timing. You'll spot problem clients before they damage your business. You'll negotiate from strength because you know exactly when you need payment versus when you'd like it.

Most importantly, you'll stop that anxiety-driven bank balance checking. When you can forecast cash flow from invoices accurately, daily fluctuations become less stressful. You know what's coming.

Your week one implementation checklist

Start this Monday. Don't wait for the perfect system.

-

Export all outstanding invoices to a spreadsheet

-

Add columns for

Due Date, Days Overdue, Promise Date, Partials Received

-

Create three aging brackets

0-30, 31-60, 60+

-

List your top 10 clients by invoice volume

-

Note their last three payment times

-

Calculate average days to payment for each

-

Create weekly forecast buckets for the next 4 weeks

-

Assign probabilities based on due dates and payment history

-

Sum expected cash by week

-

Set reminder to repeat next Monday

Week two, add promise reliability scoring. Week three, add partial payment patterns. Week four, compare forecast to actual and adjust.

The perfect forecast model doesn't exist. A simple one you actually use beats sophisticated analysis you ignore. Your invoices already contain everything needed to predict cash flow. You just need to extract the right signals and observe them consistently.

Build the discipline now, while your invoice volume is manageable. The same model that works for five outstanding invoices scales to fifty with minor adjustments. The patterns you learn about your clients become more valuable as your business grows.

Start with the checklist above. Run it weekly for a month. Then decide if 20 minutes every Monday is worth knowing your cash position 30 days out. For most solopreneurs, it's the highest ROI operational habit they'll develop.

Ready to streamline your billing process?

Join 5,000+ businesses using Billoly to reduce billing delays, automate payments, and grow revenue efficiently.