Most small businesses treat collections like a game of chicken. Send an invoice, wait, send a reminder, wait longer, maybe call, eventually write it off. The businesses that actually recover their money follow a completely different playbook—one with specific timings, predetermined scripts, and clear escalation triggers.

Working with dozens of small consulting firms and service businesses, a clear pattern emerges. The businesses recovering 70-80% of overdue payments aren't nicer or pushier. They follow a systematic escalation process that removes emotion and guesswork.

The 14-day window that determines everything

Collections success follows a brutal timeline. Payment recovery rates drop fast:

-

1-14 days overdue

85% recovery rate

-

15-30 days

62% recovery

-

31-60 days

41% recovery

-

61-90 days

23% recovery

-

90+ days

11% recovery

A marketing consultant in Austin tracked their invoices for 18 months and confirmed this pattern. Once payments crossed the 30-day mark, recovery required 3x the effort for half the success rate. Everything pivots on catching delinquencies before they age past that point.

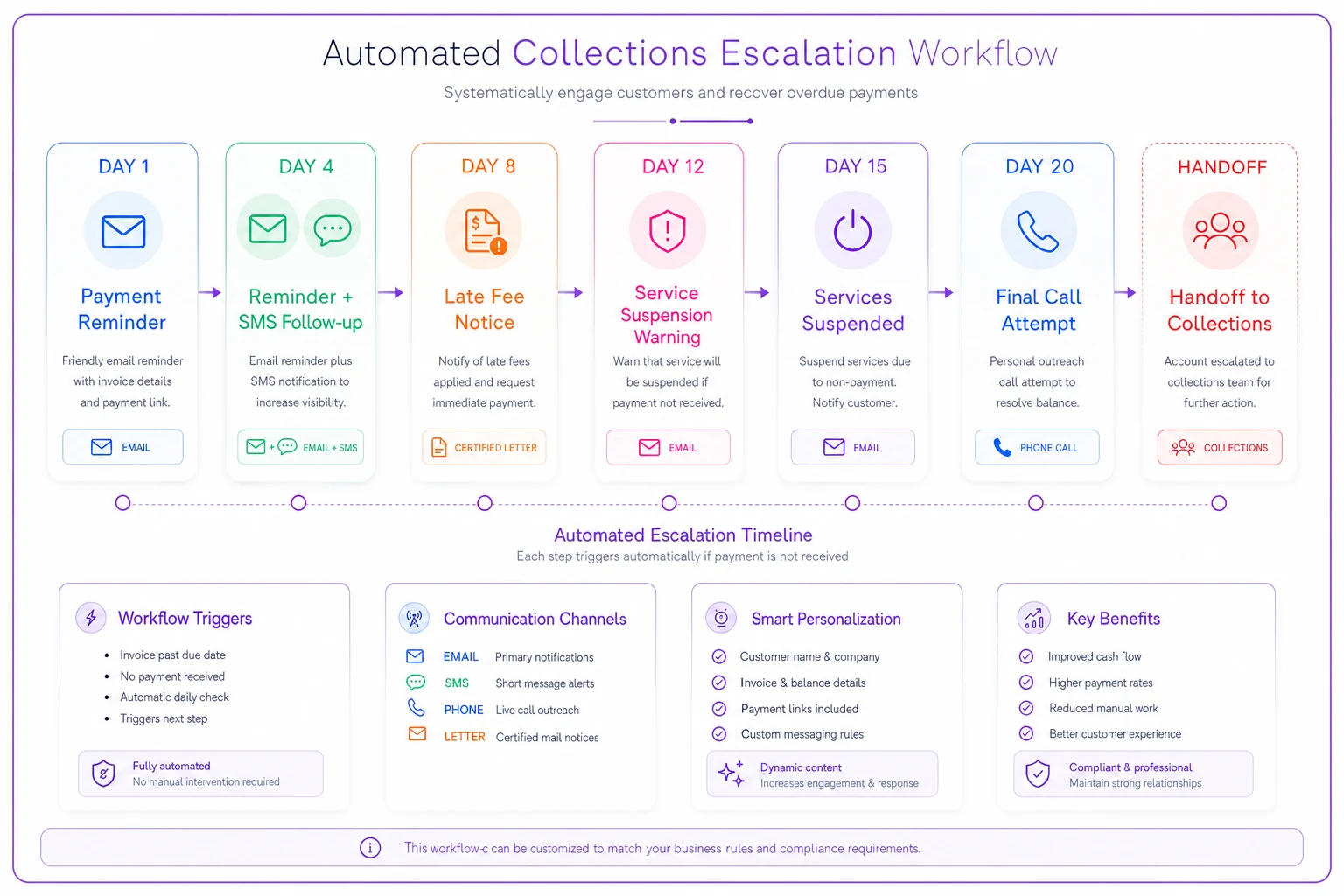

The fastest recovering businesses start their escalation process immediately. Not after "giving clients time" or "being understanding." Day 1 overdue triggers the first action.

Your escalation ladder (with exact timing)

Day -3: Pre-due reminder

Stop chasing payments and start automating your billing.

Billoly empowers you to create, send, and track invoices effortlessly while maintaining professional client relationships.

- Customizable invoice templates

- Automated payment reminders

- Real-time payment tracking

No credit card required

Channel: Email Tone: Friendly service reminder Script: "Quick heads up—Invoice #2847 for $3,400 is due Thursday, March 14th. Payment details are attached. Let me know if you need anything adjusted before then."

This isn't collections yet. It's prevention. About 22% of late payments happen because clients literally forgot or misplaced the invoice.

Day 1: Immediate acknowledgment

Channel: Email Tone: Assumptive/helpful Script: "Looks like we haven't received payment for Invoice #2847 ($3,400) that was due yesterday. If you already sent it, please forward the confirmation. If not, here's the quickest way to process it: [payment link]. Need to discuss payment timing?" Notice the assumptive close—you're assuming they want to pay, just helping them do it faster.

Day 4: Workflow check

Channel: Email + SMS Tone: Problem-solving Email: "Following up on Invoice #2847. Sometimes payments get stuck in approval workflows. Who should I contact directly in accounting to help push this through?" SMS (if you have permission): "Quick check on Invoice #2847—should I reach out to someone specific in accounting to help process the $3,400 payment?" This positions you as helping them solve an internal problem, not demanding money.

Day 8: Consequence introduction

Channel: Email Tone: Professional but direct "Invoice #2847 is now 8 days overdue. Per our agreement, late fees of 1.5% monthly begin accruing on day 10. The current balance of $3,400 will increase to $3,451 if payment isn't received by [date]. I'd rather avoid these charges. Can we schedule a 5-minute call today to resolve this?" You're introducing consequences while still offering an out.

Day 12: Service suspension warning

Channel: Email + certified letter (for amounts over $5k) Tone: Final professional attempt "This is a formal notice that Invoice #2847 remains unpaid after multiple attempts to collect. If payment of $3,451 (including late fees) is not received within 48 hours, we will:"

-

Suspend all active services

-

Hold all deliverables

-

Begin formal collections procedures

Please contact me immediately at [phone] to avoid service disruption.

Day 15: Suspension execution

Channel: Email Tone: Matter-of-fact "Per our previous notices, services have been suspended due to non-payment of Invoice #2847. To reactivate services and receive held deliverables, please remit $3,468.53 (original amount plus accrued late fees). This account will be transferred to collections on Day 20 if no payment arrangement is made."

Day 20: Final internal attempt

Channel: Phone call (documented) + Email Tone: Last chance Call script: "This is [name] from [company]. I'm calling about your seriously overdue account before it goes to collections tomorrow. The balance is $3,486.07. Can we process payment right now over the phone to avoid collections?" If no answer, leave voicemail and send email documenting the call attempt.

Day 21: Third-party escalation

Transfer to collections agency or small claims preparation.

The scripts that actually get responses

Generic templates get ignored. These work because they trigger specific psychological responses:

The "Mutual Problem" Script (Days 4-8)

"I noticed Invoice #2847 hasn't cleared yet. I'm guessing it's stuck somewhere between approval and accounting? I've seen this happen when [specific scenario]. Who's the best person to loop in to unstick this? Happy to send them documentation directly."

You're not attacking—you're acknowledging their internal friction and offering to help.

The "Protect the Relationship" Script (Days 8-12)

"We've worked together for [timeframe], and I value that relationship. Invoice #2847 is creating an awkward situation I'd like to resolve before it affects our working relationship. Can we hop on a quick call to figure out a path forward?" This leverages relationship equity before burning it.

The "Choice Architecture" Script (Days 12-15)

"I need to resolve Invoice #2847 by EOD tomorrow. I can offer two options:"

-

Full payment today with late fees waived ($3,400)

-

50% payment today, 50% in 10 days, with late fees ($1,750 today, $1,718 in 10 days)

Which works better for your current cash flow? People respond better to choosing between options than demands.

When to break your own rules

Standard escalation assumes a rational non-payer. Reality includes three categories that need different approaches:

The Genuine Crisis Client

Signs: Apologetic, communicative, provides specific timeline Approach: Payment plan with clear terms

A video production company had a client whose biggest customer declared bankruptcy, creating immediate cash flow crisis. Instead of escalating, they created a 6-month payment plan with 25% upfront. Full amount recovered.

The Dispute Manufacturer

Signs: Suddenly finds "quality issues" after receiving collection notices Approach: Document everything, escalate faster

These clients weaponize disputes to avoid payment. Skip friendly reminders. Go straight to formal documentation. Every communication in writing. Prepare for small claims from day 1.

The Serial Ghoster

Signs: No response to any communication channel Approach: Skip to Day 12 tactics by Day 6

Some clients use silence as strategy. Compress your timeline. Service suspension warnings by Day 6, execution by Day 10, collections by Day 15.

SMS escalation (when email fails)

SMS hits different than email. Use strategically:

Day 1 SMS: Don't use it yet—too aggressive

Day 4 SMS: "Quick invoice question—should I contact someone in accounting directly about #2847?"

Day 8 SMS: "Invoice #2847 hits late fees tomorrow. Here's the payment link to avoid charges: [link]"

Day 12 SMS: "Services suspend in 48 hours for Invoice #2847. Call me at [phone] to prevent disruption."

Keep SMS short, specific, and action-oriented. Include invoice numbers and amounts. Always provide immediate action path.

The portfolio management matrix

When juggling multiple overdue accounts, you need triage rules:

| Amount Owed | Days Overdue | Client History | Action Priority |

|---|---|---|---|

| >$5,000 | Any | Any | Immediate escalation |

| $2,000-5,000 | >7 days | New client | High priority |

| $2,000-5,000 | >7 days | Good history | Modified approach |

| <$2,000 | <14 days | Any | Standard escalation |

| <$2,000 | >14 days | Poor history | Consider write-off vs. effort |

| Any amount | >30 days | Any | Collections or legal |

A freelance designer managing 12 overdue accounts realized she was spending 80% of collections time on amounts under $500. Shifting focus to accounts over $2,000 improved recovery dollars by 3x with half the effort.

Third-party collections trigger points

Small businesses wait too long to involve third parties. When to pull that trigger:

Immediate collections referral:

-

Client has NSF checks

-

Client disputes after ignoring payment requests

-

Client threatens legal action

-

Amount exceeds $10,000

30-day collections referral:

-

No response to any communication

-

Partial payment with no follow-through

-

Broken payment plan

Small claims instead of collections:

-

Amount between $2,500-7,500

-

Clear contract documentation

-

Local jurisdiction

-

Client has assets

Collections agencies typically take 25-40% of recovered amounts. Small claims court costs $50-200 to file but you keep everything recovered. The math usually favors small claims for amounts under $7,500 if you have good documentation.

The payment plan framework

Maximum term: 3 months (6 for amounts over $10k) Minimum down payment: 33% Documentation: Written agreement before first payment Penalty clause: Entire balance due immediately if any payment missed

Sample payment plan agreement:

-

"Client agrees to pay outstanding balance of $4,200 for Invoice #2847 as follows:"

-

$1,400 upon signing (Date

___)

-

$1,400 on April 15, 2024

-

$1,400 on May 15, 2024 Missing any payment makes entire remaining balance immediately due. Late payments accrue 1.5% monthly interest. Client agrees to pay reasonable collection costs if default occurs.

Get signature before accepting first payment. Otherwise you're just hoping.

What to track (and why most don't)

Most small businesses never analyze their collections performance. Track these metrics monthly:

-

Recovery rate by age bucket

-

Average days to payment after first notice

-

Response rate by communication channel

-

Time invested vs. amount recovered

One consultant discovered email reminders had 12% response rate while SMS had 67%. Tuesday morning calls worked 3x better than Friday afternoons. You won't know your patterns without tracking them.

The automation advantage

Operational software changes everything here. Instead of manually tracking overdue accounts across spreadsheets and sticky notes, automated workflows handle the entire escalation ladder. Day 1 triggers the email. Day 4 triggers email plus SMS. Day 8 introduces late fees automatically.

Businesses seeing highest recovery rates use AI-powered platforms that centralize invoice status, automate reminder sequences, and escalate based on predetermined rules. No emotion. No forgetting. No uncomfortable mental burden of "should I follow up again?" The workflow runs itself.

This visual maps the escalation triggers described above.

Automate approval-path checks to reduce Day 4 friction—tag invoices with approver contacts so outreach goes to the right person immediately.

But automation only works with the right underlying strategy. Bad escalation tactics automated just fail faster.

Common escalation mistakes that kill recovery

Starting too soft: "When you get a chance" or "No rush" in early communications signals the payment isn't urgent. Every message should include specific dates and amounts.

Escalating too slowly: Waiting 30 days to make first contact drops recovery probability below 50%.

Inconsistent communication: Sending three emails in three days, then nothing for two weeks confuses the situation.

No clear consequences: Vague threats like "further action" mean nothing. Specify exactly what happens and when.

Resetting the clock: Client makes $100 payment on $3,000 bill and you restart your timeline. Partial payments shouldn't reset escalation unless part of formal payment plan.

Making collections systematic, not personal

The biggest barrier to effective collections isn't tactics—it's emotion. Small business owners take non-payment personally. They avoid confrontation. They make excuses for clients.

Professional recovery requires removing yourself from the equation. It's not about being mean or nice. It's about following a documented process that protects your business's cash flow.

Build the escalation ladder. Write the scripts. Define the triggers. Execute without deviation.

Every day you delay costs money. Every exception you make trains clients to pay late. Every emotional decision undermines the process. That's how small portfolios recover big dollars.

Ready to streamline your billing process?

Join 5,000+ businesses using Billoly to reduce billing delays, automate payments, and grow revenue efficiently.